Yeah folks, we've been doing some research on retirement. Everybody's always talking about the rate of return. Is it important when you retire? Right? Of return, rate of return, how much are you making on your mutual fund? How much are you making on your bank IRA? How much do you make? What is your interest rate? What's your rate of return? What's your rate of return? What's your rate of return? And you know, it matters a lot whether you get ten or ten and a half. Or it matters a lot whether you get 11 or whether you do an inflation-adjusted or inflation and expense-adjusted calculation. And all this, you know, all these nerds in my business world and my lot in the financial space – and myself included when I was a young guy – we spent an inordinate amount of time, money, and brainpower wearing our little nerd calculators out over a tenth of a point here or there. And you know what? We're actually finding now, in the current research, the best research that's being done in the retirement space right now. You know what the number one factor about whether you retire with dignity and have enough money to retire is? It is not the rate of return. It is not whether it's tax-free or tax deferred. It is not whether it's a 401k or a Roth 401k. It's not whether it's a traditional IRA or Roth IRA. It's not whether you use a 457 or whether you use an annuity. It's not the type of product. It's not the return. It's not the tax position of it. None of that is the main indicator of whether you retire with money in your account to retire on. You know what the main indicator is?...

Award-winning PDF software

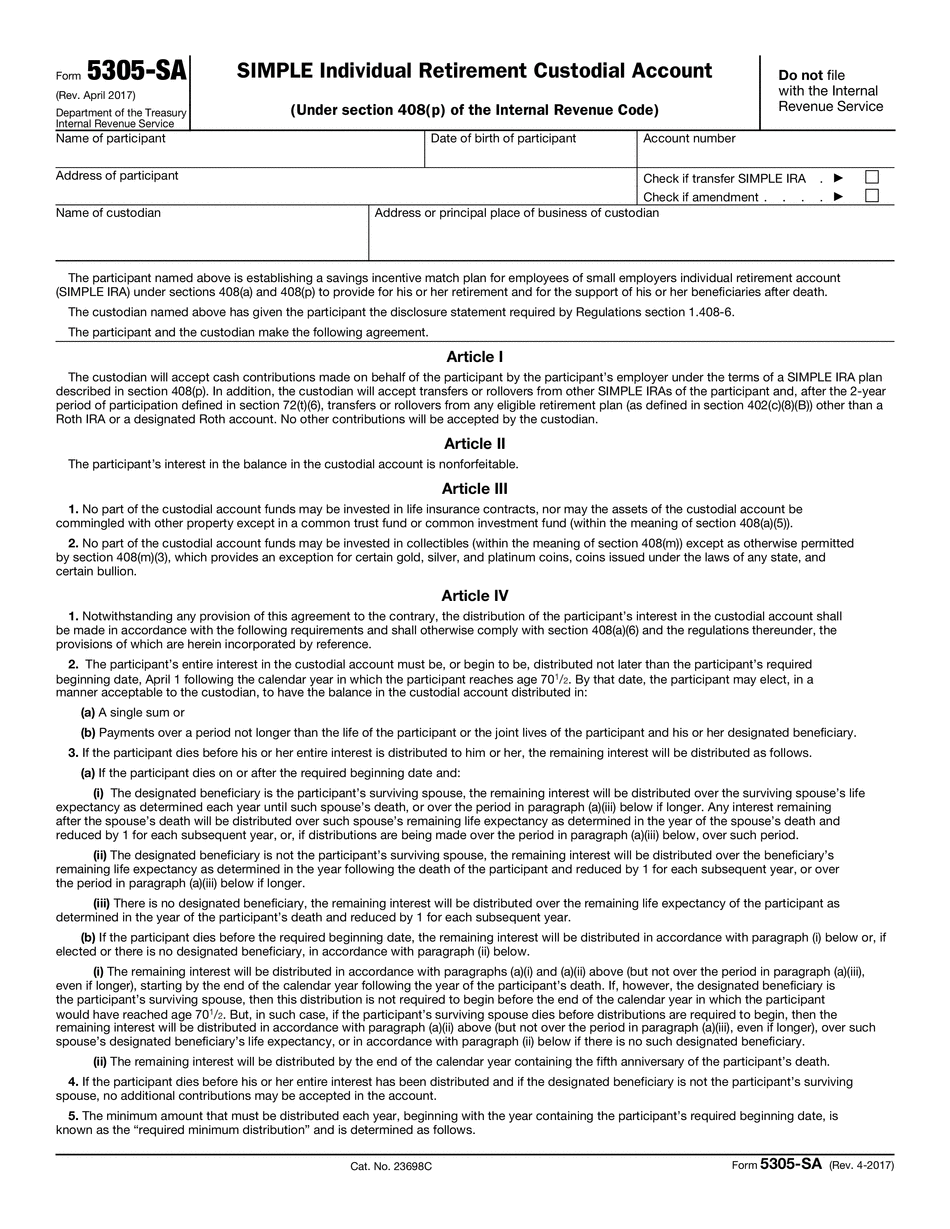

Sep ira irs 5305 Form: What You Should Know

Agreement) If you make a contribution under section 408(g)(4) of the Internal Revenue Code during the year, this is not a SEP contribution. The SEP is a non-deductible deposit that isn't subject to the usual contribution laws, such as taxable contributions and income limits and prohibited deferral rules. You must use Form 5305-SEP to establish the SEP Plan and receive SEP benefits if the SEP was part of a plan prior to Jan 3, 2022. SEP Plan — IRA—Internal Revenue Code (a) The individual has attained the age of 59 1/2 years as of the close of the plan year for which the plan is established. (b) The plan satisfies the requirements in paragraph (c) of this section, except that: 1. A portion of the contributions must be made during the tax year that includes the earliest of-- (i) The anniversary of the plan year of the beginning of the plan, for contributions made within taxable years of the plan; or (ii) The plan year of the IRA beneficiary's attainment of age 70 1/2; and 2. The portion of the contributions that is taken into account under paragraph (c)(3) of this section has been made by the end of the tax year that includes all contributions to the SEP Plan. The portion of the contributions that is taken into account under subparagraph (E) of paragraph (b)(2) of this section is based on the total salary deferral amount, computed under paragraph (b) of this section and paragraph (d) of section 401(a): For all pay periods beginning on or after Jan. 20, 2022, but before January 3, 2023, if the participant's salary is 1,000,000 or more, the portion of employer contributions required under subparagraph (E)(i) of this paragraph (b) is equal to 3/4 of the participant's salary for that year for Social Security tax purposes. For all pay periods beginning on or after Jan.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5305-Sa, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5305-Sa online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5305-Sa by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5305-Sa from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Sep ira irs 5305