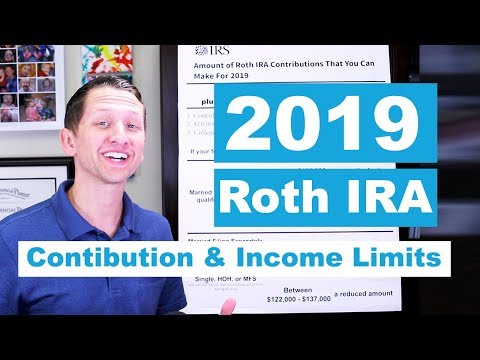

Today, I'm going to talk about the Roth IRA contribution limits for 2019. I'm also going to go over some facts and figures, such as how much you can save, when to save, and how to save. If this is your first time at our channel, or you haven't subscribed, click on the subscribe button at the bottom. My name is Travis Sickles, a certified financial planner with Sickleson Financial Advisors. Let's start out by talking about what a Roth IRA is and how it works. It is a retirement account where you can put in earned income, which are dollars that you're earning from a paycheck. These dollars are put directly into the Roth IRA with after-tax dollars, which are the dollars that you're getting from your paycheck. They will grow tax-deferred and hopefully come out a hundred percent tax-free in retirement. Now, there are a couple of ways that you can pull out money from the Roth IRA early, but I will go over that in just a minute. Let's first talk about the contributions or the changes for 2019. As you can see on the board, contribution limits have increased by $500 to $6,000. In 2018 and prior, it was $5,500 per year. Now, if you're 50 and over, you can contribute an extra $1,000, bringing the total to $7,000. It's important to note that it's 50 and over, not over 50, so if you're 50 or older, you can contribute an additional $1,000. That's the maximum contribution. Now, what is a Roth IRA good for? There are three things that I've pointed out here. Anything you put into the Roth IRA, you can pull out. This is called your contributions or your principal. So, if you put in $500 today, and in two weeks you want to pull that...

Award-winning PDF software

Simple ira contribution deadline 2025 Form: What You Should Know

Form 5498 — IRA Contribution Information — Tax Act Form 5498 should be mailed to you by May 31st to show traditional IRA contributions made for the prior year between January 31st of the prior year and the tax Form 5498 — IRA Contribution Information — Tax Act If you don't receive either form from your custodian by May 31st, you must file the proper form on your tax return to have taxes paid for 2018. If you've already filed your tax return on time, don't file a Form 5498 with the IRS. For those that need help filing the Form 5498, the IRS has a good IRS Form The IRS may ask for all sorts of information and documents from you to prepare for its March 1, 2018, filing deadline.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5305-Sa, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5305-Sa online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5305-Sa by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5305-Sa from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Simple ira contribution deadline 2025